California's rideshare industry has revolutionized transportation in the state and around the world, with millions of residents using services like Uber and Lyft daily. However, with this growth comes complex insurance requirements that many drivers and passengers don't fully understand. If you've been involved in a rideshare accident, our experienced Uber and Lyft accident attorneys will help you understand your rights and coverage options under California law.

What Are California Rideshare Insurance Requirements

California's rideshare insurance requirements exceed those in most states. The state requires higher liability insurance limits for rideshare drivers waiting for a ride request compared to many other jurisdictions. These enhanced standards ensure better protection for accident victims and provide comprehensive coverage throughout all phases of rideshare activity.

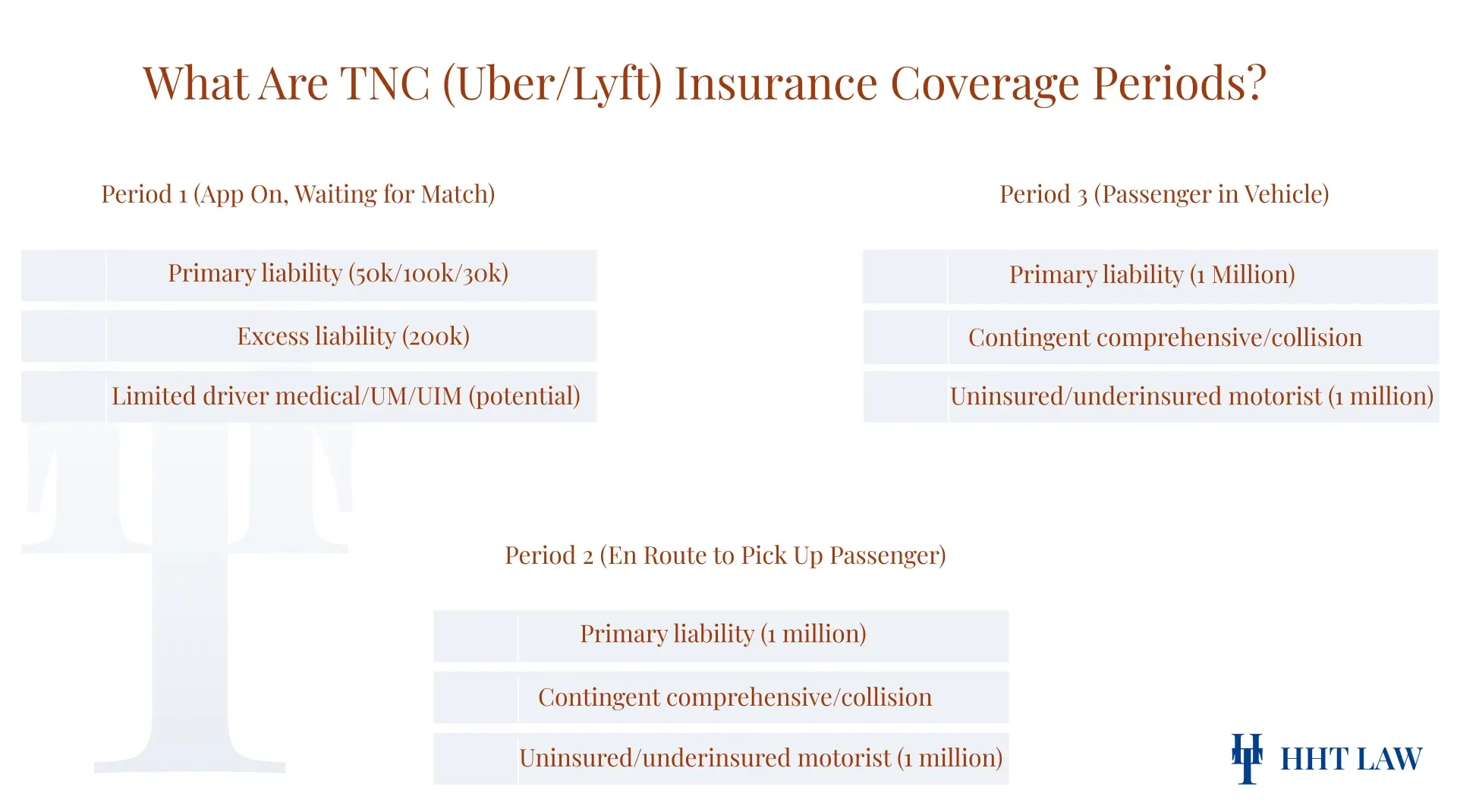

California Public Utilities Code Section 5433 establishes specific insurance requirements for transportation network companies (TNCs) that vary based on three distinct periods of rideshare activity:

- Period 1: app on, waiting for match: During this phase, when rideshare drivers have logged into the TNC app but haven't accepted a ride request, California law requires primary insurance coverage of at least $50,000 for death and personal injury per person, $100,000 for death and personal injury per incident, and $30,000 for property damage. Rideshare companies and their drivers must also maintain excess coverage of at least $200,000 per occurrence to cover additional liability.

- Period 2: en route to pick up passenger: Once a driver accepts a ride request and is traveling to pick up the passenger, the rideshare driver’s insurance must be primary and provide $1 million in coverage for death, personal injury, and property damage.

- Period 3: passenger in vehicle: From the moment the passenger enters the vehicle until they exit, the rideshare company and driver must provide $1 million in liability coverage and $1 million in uninsured/underinsured motorist coverage.

How California Rideshare Insurance Law Protects You

The state's comprehensive approach addresses coverage gaps that exist in many other jurisdictions and provides clear guidelines for when different insurance policies apply.

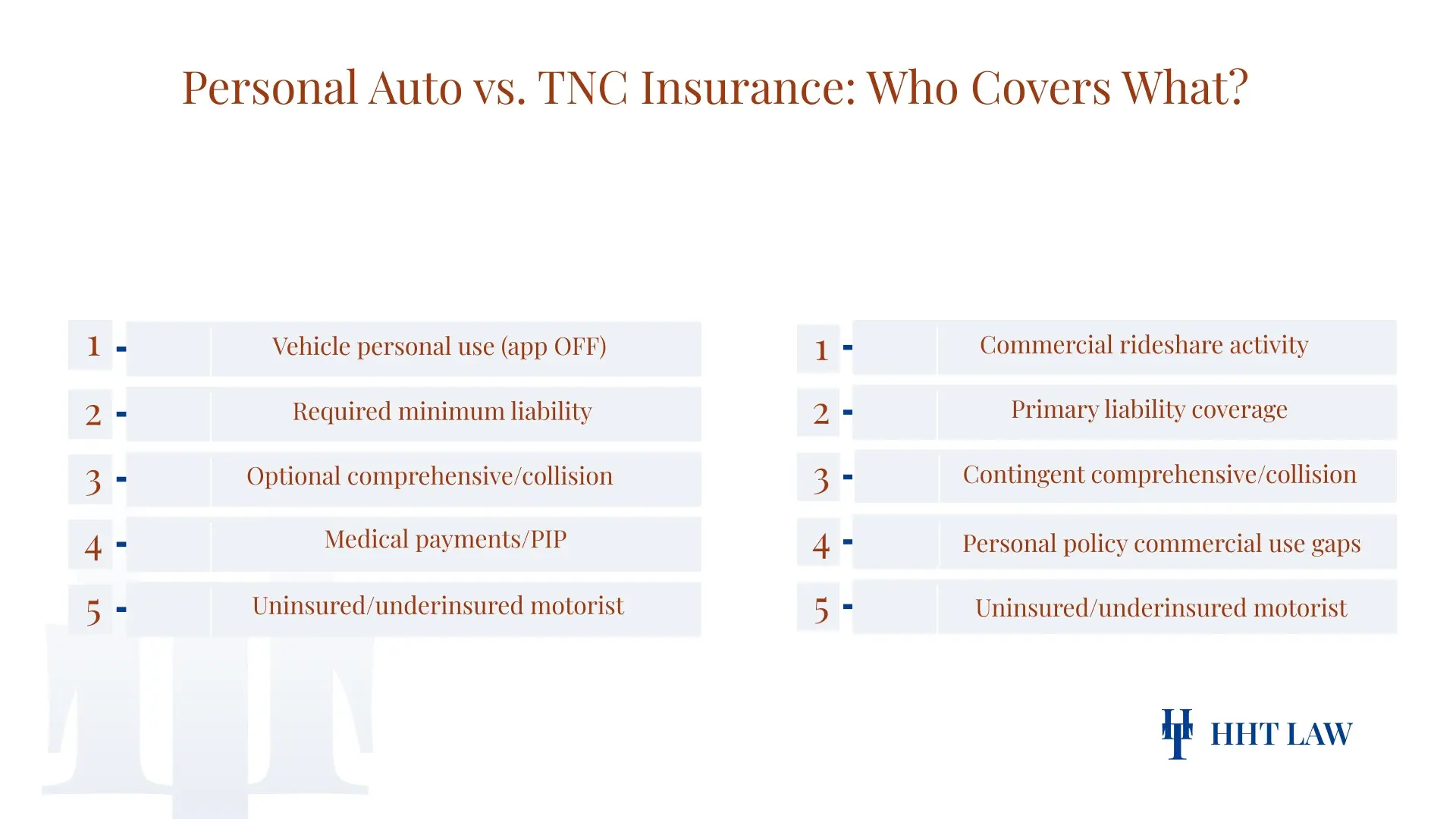

Personal Auto Insurance vs. Rideshare Insurance

Regular personal auto insurance policies typically exclude coverage when using a vehicle for commercial purposes, such as driving for a rideshare service. This is where California rideshare insurance law steps in to fill coverage gaps.

Coverage under transportation network company insurance policies cannot be dependent on personal automobile insurance first denying a claim, nor can personal automobile insurance be required to first deny a claim. This provision ensures that accident victims don't face delays in obtaining compensation due to disputes between insurance companies.

Assembly Bill 2293: The Foundation of California's Rideshare Insurance Law

Assembly Bill 2293, signed into law by Governor Jerry Brown in September 2014, established the comprehensive regulatory framework for rideshare insurance in California. The law went into effect on July 1, 2015, requiring ride-share drivers and companies to have liability insurance coverage during all three periods of rideshare activity.

This groundbreaking legislation addressed critical insurance gaps that previously left drivers and passengers vulnerable. The law established a "personal insurance firewall" to ensure personal auto insurance policyholders would no longer subsidize commercial TNC activities.

Insurance Coverage Requirements for Different Situations

California law establishes specific insurance requirements that vary depending on the type of coverage needed and the circumstances of rideshare operation.

Liability Coverage Standards

California law mandates specific liability coverage amounts for rideshare drivers. As of January 2025, California increased its minimum liability insurance requirements for all drivers, including rideshare drivers. However, rideshare drivers must meet higher standards than regular motorists.

For personal auto insurance policies, California's minimum coverage increased from 15/30/5 to 30/60/15 in January 2025. This means $30,000 per person for bodily injury, $60,000 per accident for bodily injury, and $15,000 for property damage.

Comprehensive Coverage and Collision Insurance

Uber provides comprehensive and collision coverage with a $2,500 deductible during periods 2 and 3, provided drivers maintain collision coverage on their personal auto insurance policy. Lyft also provides comprehensive and collision coverage with a $2,500 deductible under the same conditions.

This contingent coverage model means rideshare drivers must maintain their own comprehensive and collision insurance to access the rideshare company's coverage during active periods.

Uninsured and Underinsured Motorist Protection

Both Uber and Lyft provide drivers with $1 million of bodily injury coverage for uninsured and underinsured motorists during periods 2 and 3. This protection is necessary in California, where many drivers carry only minimum insurance that may not cover serious accidents.

What Rideshare Drivers Need to Know About Insurance Maintenance

Drivers must navigate the complex relationship between their personal insurance policies, TNC-provided coverage, and California's specific regulatory requirements to ensure they're properly protected at all times.

Personal Insurance Policy Requirements

California law requires all rideshare drivers to display their company's decal in the vehicle's windows at all times when the app is active. Additionally, drivers must maintain their personal auto insurance policy to complement TNC coverage.

Nearly half of all rideshare drivers don't have a rideshare endorsement in their personal auto policy, often because they don't know they need one. This gap can leave drivers financially vulnerable if their personal insurance denies claims for commercial use.

Commercial Insurance vs. Rideshare Endorsements

Rideshare drivers in California have several options to meet insurance requirements:

- Rideshare Endorsement Adding a rideshare endorsement to your personal auto policy typically costs an average of $17 per month in California.

- Commercial Coverage Full commercial insurance policies provide comprehensive protection but are significantly more expensive.

- TNC-Provided Coverage Relying solely on the rideshare company's insurance, though this may leave gaps in coverage.

Insurance Companies Offering Rideshare Coverage

The California Department of Insurance has approved new insurance products from companies like Farmers Insurance and Metromile to cover rideshare drivers during the pre-match period. Clearcover offers some of the most affordable rideshare insurance in California, averaging $112 per month for full-coverage auto insurance with rideshare coverage.

Understanding Insurance Claims After Rideshare Accidents

California's regulatory framework provides specific guidelines for how insurance claims should be handled, but understanding your rights and the process can help ensure you receive proper compensation.

When Rideshare Insurance Applies

In every instance where the rideshare company insurance maintained by a participating driver has lapsed or ceased to exist, the transportation network company must provide the required coverage beginning with the first dollar of a claim. This provision ensures continuous protection even if a driver's personal insurance lapses.

Medical Expenses and Property Damage Coverage

Rideshare companies provide insurance coverage from the moment a driver turns on the rideshare app until the passenger exits the vehicle, including $1 million liability insurance that covers passengers regardless of who caused the accident.

For rideshare drivers, medical expenses coverage varies by period:

- Period 1: Limited coverage, primarily liability protection for other parties.

- Periods 2 & 3: Comprehensive medical coverage through the TNC's $1 million policy.

Lost Wages and Compensation

When rideshare accidents result in serious injuries, victims may be entitled to compensation for lost wages, medical expenses, and pain and suffering. California Assembly Bill 2293 requires TNCs to maintain a $1 million insurance policy that covers personal injury, property damage, and death, plus $1 million in uninsured and underinsured motorist coverage.

What to Do After a Rideshare Accident

Taking the right steps immediately after an accident can protect your rights and help ensure you receive proper compensation for any injuries or damages you've suffered.

Immediate Steps

- Seek Medical Attention Your health and safety are the priority.

- Document the Scene Take photos and gather witness information.

- Report the Accident Contact law enforcement and the rideshare company.

- Preserve Evidence Keep all documentation related to the accident.

- Contact an Experienced Attorney Rideshare accidents involve complex insurance issues that require professional guidance.

Insurance Information to Collect

After a rideshare accident, collect:

- The driver's personal insurance information

- The rideshare company's insurance details

- Information about which period the accident occurred in

- Documentation of any injuries or property damage

Understanding Fault and Liability

California's Proposition 22, upheld by state courts in March 2023, classifies app-based drivers as independent contractors rather than employees. This means that after an Uber or Lyft accident, it's generally not possible to hold the rideshare company vicariously liable for driver mistakes.

However, rideshare companies still maintain substantial insurance coverage that may apply depending on the circumstances of the accident.

Protecting Your Rights Under California Rideshare Insurance Laws

The interplay between personal auto insurance, TNC insurance, and California's enhanced requirements creates a robust safety net, but only when properly understood and utilized. From the minimum liability coverage requirements to the million-dollar policies protecting passengers, California law ensures that accident victims have access to compensation when needed.

Contact us today to discuss your case and learn how we can help you secure the compensation you deserve under California rideshare insurance law.